Article excerpt http://bbs.51touch.com/

TechNiche: In-cell touch likely

becomes a reality in 2012

In this issue of TechNiche, we look at 1) recent findings from

channel checks 2) handset/tablet supply chain revenue update

3) PC market update. Based on our recent channel checks, we

believe that in-cell touch display may start mass production by

mid-2012. The timing appears to be coincidental to the widely

expected iPhone 5 launch in 2H12. TPK may risk loosing orders

earlier than expected. Our channel checks also indicated a

better-than-expected iPhone 4s but a weaker iPad 2 sell-

through after the Thanksgiving holiday weekend. 4Q

notebook shipment was weaker-than-expected, not because

of HDD shortage but due to weaker end demand. HDD

shortage is having a big impact on the DIY motherboard

market because smaller players have no bargaining power

to get HDD supply or they have to pay 2-3x price premium

to get it in the channel.

» In-cell touch display to put TPK at risk

We believe in-cell technology mass production may start sooner than

expected in mid-2012. Apple’s patent on integrated touch screen was

published in August 2011 (see Appendix) and the company may

outsource the technology to display makers to make the product. As a

result, TPK’s risk of loosing orders in 2H12 is increasing.

» Better-than-expected iPhone 4s and weaker iPad2

Our channel checks after the Thanksgiving weekend indicate that

iPhone 4s sell-through seems to be better than expected, while iPad 2

was weaker.

» PC Update: Cutting 4Q11 notebook and motherboard

shipments

The impact of HDD shortage appears to be more pronounced in the

DIY motherboard market as smaller players have less bargaining

power to get HDD supply. We are cutting our Taiwan motherboard

shipment forecast to -19% QoQ from -11% in 4Q as a result. We also

cut our 4Q notebook shipments to -4% QoQ from a flat quarter on

weak demand.

» Most companies under our coverage in Taiwan are either

missing or at the low end of their guidance for 4Q except

Wistron and Flexium

Wistron notebook shipment is expected to grow 6% QoQ in 4Q11,

beating its guidance of 0-5% growth. Flexium’s 4Q11 revenue is now

on track to reach more than 20% QoQ, beating its guidance of a flat

quarter.

1. Recent Channel Checks

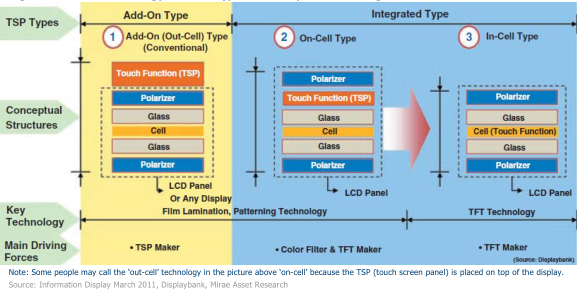

In-cell Touch Technology for iPhone 5?

Our channel checks indicate that Apple is pushing very hard to make in-cell touch panel technology to become a reality. Mass production of in-cell touch TFT-LCD display may come as early as mid-2012 and the timing appears to be coincidental to the next iPhone (widely expected as iPhone 5) launch in 2H12.

Similar to Apple’s cooperation with TPK on its first-generation touch panel, the patent of the upcoming in-cell touch technology may be owned by Apple (see Appendix). We believe Apple can license it to different display companies to do the manufacturing for Apple. Therefore, the risk of order loss at TPK in 2H12 has increased significantly when in-cell touch TFT-LCD mass production becomes available.

As we highlighted in our initiation report dated 23 November 2011, TPK may become a ‘lamination’ company for the touch panel because an in-cell touch TFT-LCD display still needs to be laminated with the cover glass to ensure that the whole module functions properly. But the total available market will be greatly reduced for TPK. Instead of doing two layers of lamination plus the touch sensors (50% or more of TPK’s touch sensors are outsourced), TPK can only do one layer of lamination when in-cell touch display is fully ramped. We estimate that the total available gross profit from a laminated in-cell touch display module will be reduced by roughly two-thirds as a result.

We expect the in-cell technology will only be used for displays in smartphones initially. It will probably take at least another year or two before it can be implemented on tablet-sized displays with acceptable yield, in our view.

Figure 1. In-cell technology vs. other types of touch panel technologies

iPhone 4s appears to be better-than-expected but iPad 2 was weak

Our channel checks indicate that iPhone 4s sales were better than expected but iPad 2 may be weaker than expected after the Thanksgiving holiday weekend. The weakness in iPad 2 may be due to strong price competition from Kindle Fire as well as other tablet makers cutting prices to clear inventory. This has a negative implication on Simplo (because of its iPad 2 exposure and weakness in notebooks). We believe that Simplo will likely come in at the low end of its 4Q11 guidance or may even miss the guidance slightly. If its December non-consolidated comes in at around NT$4bn, it will be at the low end of the 4Q revenue guidance of NT$13bn.

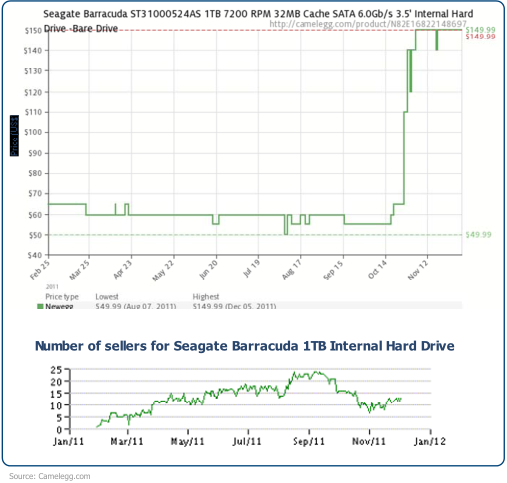

High HDD price turning customers away in the DIY PC market

HDD price in the channel has increased by 2-3x since the Thailand floods in October and PC makers have raised prices for some of their PCs. Out of the ~170m HDD demand in 4Q11, both Seagate and Western Digital said that nearly 120m will be supported. We estimate that PC demand is only 90m+ in 4Q11 and therefore, most of the leading PC brands will have their HDDs supported. The most affected areas are those smaller players in the channel (for the DIY market and data backup market) as well as those in the consumer electronic market (e.g. HDDs for camcorders or TV recording).

Figure 2. Price and no. of sellers of Seagate Barracuda 1TB Internal Hard Drive

Our latest checks indicate that the surge in HDD price has slowed down the demand for desktop PCs in the DIY market. Since most of the people who participate in the DIY market are system integrators and PC ‘experts’, we believe many of them have chosen to wait rather than paying a high price for HDD. We noticed that the motherboard market in Taiwan (mostly for the DIY market) has slowed down dramatically as a result. After the floods in Thailand in October, Taiwan motherboard shipments dropped 20% MoM on the same month, deeper than the 15% MoM drop in October 2010. In November, we estimate that motherboard shipments only grew by 4% MoM, also lower than the 10% MoM growth in the same month a year ago.

One of the motherboard makers believes that HDD price in the channel may come down in late December and early 2012, because too many traders have stocked up and made good money out of this ‘disaster’.

Since the supply is improving (based on the latest update from Seagate and Western Digital) and demand is coming down because of higher HDD price and low season in 1Q12, we believe that we are seeing the worst in terms of HDD shortage in the PC market in December 2011. We have passed the peak month of PC builds in October. Under normal circumstances, the run rate in a low month in 1Q is 30%+ lower than the peak month in 4Q. Since only 25-30% of the global HDD supply was affected by the Thailand floods, we may reach a short-term supply-demand balance for the PC market in late January or February. If HDD traders still do not sell their stocks on hand in December or January before the Lunar New Year, it is very likely that they will sell them at a lower price afterwards because HDD supply will only improve from now onward, although the shortage in the non-PC market may last longer.

2. Handset/Tablet Supply Chain Revenue Update

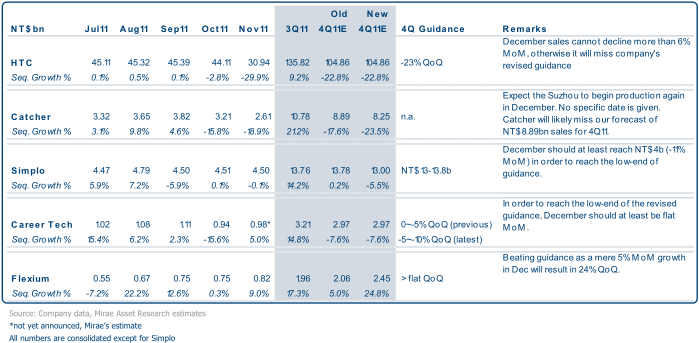

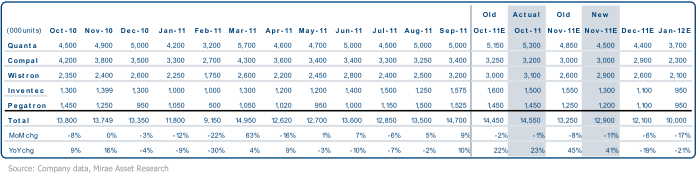

Figure 3. Handset and handset component: monthly and quarterly revenue

HTC – A sharp decline in November sales (reported at -30% MoM) is expected by the market after the company lowered its 4Q guidance on 23 November 2011. December sales have to decline less than 6% MoM in order to meet its revenue guidance of flat YoY revenue growth (i.e. ~NT$104bn).

Catcher – The 19% MoM revenue decline in November is largely in line with market expectations. The company still cannot give a date on when its Suzhou plant can resume production but it is expecting the problem to be resolved in December. Our 4Q sales forecast of NT$8.89bn is unlikely to be achieved. We believe 4Q sales could be in the range of NT$8.0bn to NT$8.5bn.

Simplo – 4Q non-consolidated sales will likely come in at the low end of its guidance of NT$13.0-13.8bn. Depending on the shipment in December, it may even miss the 4Q guidance slightly. We believe this is mainly due to weakness in notebook and iPad2.

Career Tech – The company has not announced November sales yet, but we expect it to grow 3-5% MoM. To reach the low-end of its revised revenue guidance, December sales have to be at least flat MoM. However, we believe the company is still able to grow at 7% MoM in December mainly due to the effect of order transfers from Japanese competitors (as a result of the Thailand floods). Our 4Q11 revenue estimate remains unchanged at 7.6% QoQ decline.

Flexium – November consolidated sales came in stronger-than-expected at 9% MoM mainly due to the order transfers from Japanese competitors (as a result of the Thailand floods). The momentum of the order transfers should carry on to December, so we now expect 4Q11 to grow 25% QoQ, far better than its original guidance of a flat quarter and our previous estimate of 5% QoQ growth.

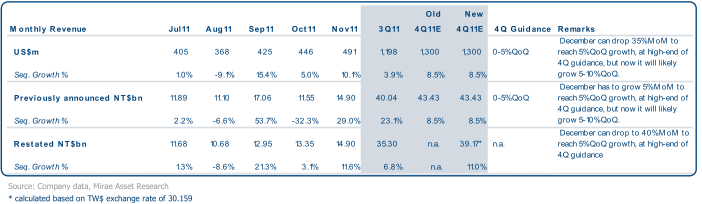

TPK – The company has restated its monthly sales (see Figure 3) because based on the old method of calculation, a fluctuation in the foreign exchange rate can lead to a huge fluctuation in monthly sales numbers in TW$.

Previous Calculation:

Monthly sales in TW$ = (Year-to-current-month accumulated sales in US$ x Month-end FX rate) - (Year-to-previous-month accumulated sales in TW$)

Re-stated Calculation:

Monthly sales in TW$ = Monthly sales in US$ x Month-end FX rate

It may be better to compare the monthly revenue in US$ terms, in our view. This can give us a true picture of the business flow, as all the businesses are done in US$. TPK will likely grow its revenue (in US$ terms) by

5-10% now versus the original guidance of 0-5% growth, which is in line with our forecast of 8.5% QoQ growth. Its December revenue now can decline 35% MoM to meet the low end of its revised guidance and 26% MoM to meet our forecast.

Figure 4. TPK previously announced vs. restated consolidated monthly revenue

3. PC Market Update

Notebook

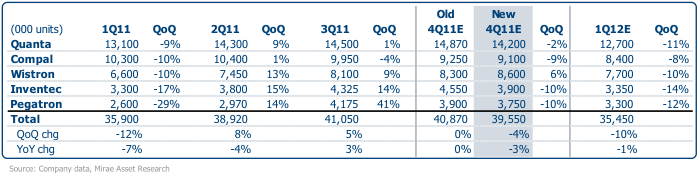

We have cut our 4Q11 notebook shipment forecast further to 4% QoQ decline, lower than our previous forecast of a flat quarter and 5-year historical average of +10% QoQ growth, mostly due to macro weakness. The notebook ODMs appear to have little impact from the HDD shortage compare to the motherboard makers, because notebook ODMs are supported by top tier brand names that have priority in HDD supply. Wistron seems to be less affected by weak demand and HDD shortage. We believe it was due to the strength in Lenovo commercial PCs. As a result, Wistron is the only notebook ODM that is likely to beat its 4Q11 guidance. The company originally guided for 0-5% QoQ growth for 4Q11 and now it will likely grow 6% QoQ.

We expect Taiwan notebook shipments to decline 10% QoQ in 1Q12, less than the 5-year historical average of 11% decline due to some pent-up demand as well as HDD supply tightness to alleviate in 1Q12.

Figure 5. Taiwan Notebook Shipment (Monthly)

Figure 6. Taiwan Notebook Shipment (Quarter)

Quanta (main customers: Apple, HP, Lenovo, Dell, Acer)

• The November notebook shipment is expected to decline 15% MoM, worse than our previous forecast of 8% decline and market consensus. We think this is because of weakness in HP consumer notebooks (HP accounts 25-30% of its shipments), rather than the impact from HDD shortage. We estimate December shipment to decline to 4.4m units following the normal seasonal pattern. October notebook shipment came in at 5.3m units, better than our previous forecast mostly because the impact of metal casing shortage from Catcher (due to the shut down of its Suzhou plant) appears to be less than we initially estimated.

• 4Q11 notebook shipments are now expected to decline 2% QoQ versus our previous forecast of 3% growth due to weaker-than-expected demand from its customers in November and December; we think this is mainly because of the weakness in HP. This implies the company will miss its 2011 notebook shipment guidance of 57m units by 2% and its 4Q11 guidance of a flat quarter.

• We expect demand to remain sluggish in January as there are less working days due to Chinese New Year (on 23 January 2012) and forecast it to drop by 16% MoM. As for 1Q12, we estimate it to decline 11%, roughly in line with its 5-year average of 12% QoQ decline.

• We also expect 4Q11 gross margin to be lower than 3Q11 of 3.7% as there is a richer mix of high-end products in 4Q11 that makes the MVA percentage smaller. The OPEX-to-sales percentage in 4Q11 is estimated to come down to 2.0-2.2% from 2.5% in 3Q11. This is largely in line with our expectation of 1.3% operating margin for 4Q11.

Compal (main customers: Acer, Lenovo, Dell)

• We maintain our November notebook shipment forecast of 6% MoM decline and December of another 3% MoM decline due to weak demand but not HDD shortage, according to the company. October notebook shipment was 3.2m units, largely in line with our forecast.

• We are now forecasting 4Q11 to decline 9% QoQ, at the low end of its 5-10% decline guidance and also lower than our previous forecast of 7% decline, due to weaker-than- expected demand from its key customers.

• January notebook shipment is estimated to drop by 21% MoM due to Chinese New Year holidays. We expect 1Q12 shipment to decline 8% QoQ, below the 5-year historical average of 4% decline because Acer is now a weaker customer than in the past few years. The decline is expected to be milder than other notebook ODMs because of a lower base in 4Q11.

• The company is maintaining its 4Q11 gross margin to be flat to 3Q11 at 5.0%. It will only start to ship ultrabooks in 1Q12.

Wistron (main customers: Dell, Lenovo, HP)

• Our November notebook shipment forecast is now better than our previous forecast by 0.3m units mainly due to better-than-expected demand from Lenovo commercial PCs, in our view. December shipment should come down to 2.6m units due to seasonal factors. October shipments came in at 3.1m units, slightly higher than our forecast due to stronger-than- expected demand.

• 4Q11 notebook shipments are now estimated to grow 6% QoQ, higher than the guidance of 0-5% growth and our previous forecast of 2% growth, due to stronger-than-expected demand from Lenovo, in our view.

• We note that Wistron is the only ODM that is expected to beat its 4Q11 shipment guidance, and appears to have little or no impact from the HDD shortage. We think the strength is coming from Lenovo and in particular its commercial PCs are getting higher priority in HDD supply.

• We expect January notebook shipment to drop to 2.1m units due to Chinese New Year holidays and 1Q12 to drop by 10% QoQ, in line with its 5-year average of 11% decline.

• The company also expects 4Q11 gross margin and operating margin to improve from 3Q11 as the TV over capacity is largely resolved, NT dollar depreciation and larger notebook scales.

• As for 2012, it expects 33-35m notebook units (10-17% YoY growth) and 3-4m tablet units (versus 1m units guided by the company for 2011) as it gains more tablet customers.

• We are only expecting Wistron to ship 32.8m notebooks in 2012. Wistron expects to gain more share from its existing customers in handheld devices in 2012.

Inventec (main customers: HP, Toshiba)

• We expect November notebook shipment to decline to 1.3m units from 1.5m in October, below our previous forecast of 1.55m. December is estimated to drop further to 1.1m units due to seasonality. We believe HP contributed to most of its weakness in the past 2 months.

• Our 4Q11 notebook shipment is now forecast at 10% QoQ decline, worse than our previous forecast of 5% gain as we were too optimistic in HP demand previously when Inventec beat market expectations in September but sales have since slowed down.

• January is expected to decline by 14% MoM and 1Q12 to drop by 14% QoQ, in line with its 5-year historical average.

Pegatron (main customer: Asus) incl. netbook

• We are slightly tweaking November notebook shipment number from 1.25m to 1.2m units, a 17% MoM decline mostly due to weakness in netbook while regular notebook remains stable. December shipment is expected to drop to 1.1m units due to seasonality. October shipment came in at 1.45m units, in line with our forecast.

• Our 4Q11 notebook shipment is now looking at 10% QoQ decline, below our previous forecast of 7% decline mainly due to weaker-than-expected demand in netbook.

• The company is guiding a decline of 10-15% in regular notebook, netbook and tablet shipments together in 4Q11 and if we include tablet shipments, we expect 4Q11 to decline 12% QoQ within the company guidance.

• January notebook shipment is now estimated to decline 14% MoM to 0.95m units due to Chinese New Year holidays. We estimate 1Q12 to drop by 12% QoQ, better than its 5-year historical average of 24% QoQ decline, as the addition of new regular notebook customers should help stabilize the quarterly pattern, in our view.

• We expect 4Q11 tablet shipment to reach 0.61m units, declining 24% QoQ due to the one-month delay (to December) in launching Transformer Prime.

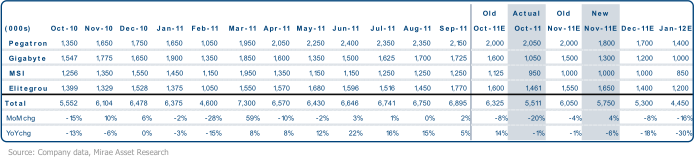

Motherboard

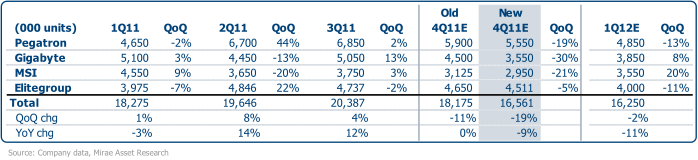

We found that the HDD shortage has a bigger impact on motherboards than notebooks, and specifically more so in the DIY market than the ODM market as the DIY market is more fragmented with players having less bargaining power. We are therefore revising down our 4Q11 motherboard estimate to 16.6m (19% QoQ decline) from 18.2m units (11% QoQ decline). Elitegroup is predominantly in the motherboard ODM market, therefore is less affected by HDD shortage and is estimated to decline the least in 4Q11. Gigabyte, which focuses on the DIY market, saw a sharp decline in October due to HDD shortage and inventory correction, which is the main reason for our downward revision in 4Q11.

However, we think the price of HDD in the channel will start to come down at the beginning of 1Q12 as HDD production recovers gradually from the flood in Thailand. As a result, we should see some pent-up motherboard demand in 1Q12, thus leading to a slightly above-seasonal quarter of 2% QoQ decline than the 5-year historical average of 3% QoQ decline.

Figure 7. Taiwan Motherboard Shipment (Monthly)

Figure 8. Taiwan Motherboard Shipment (Quarterly)

Pegatron (4938 TT, not rated)

• We are revising the November motherboard shipment down by 0.2m to 1.8m units due to the impact of HDD shortage and December should come down further to 1.7m as end customers delay purchases in light of HDD price hike. October motherboard shipment was 2m units, in line with our forecast, and declined 5% MoM due to seasonality.

• The company guided a 15-20% QoQ decline on 4Q11 motherboard shipment. We estimated a 19% QoQ decline, the lower end of the guidance, given that the HDD shortage impacted the motherboard and desktop sectors the most.

• As for 1Q12, we estimate it to decline 13% QoQ, in line with its 4-year average, as weakness in demand continues even after a worse-than-expected 4Q11. We have factored in the Chinese New Year being earlier next year and estimated a 18% MoM decline in motherboard shipment in January.

Gigabyte (2376 TT, not rated)

• We estimate November motherboard shipment to increase to 1.3m units from 1m in October as inventory fell to a more reasonable level. December is estimated to decline slightly to 1.2m units due to weakness in end market as a result of HDD price hike. The company saw a sharp decline in October motherboard shipment of 34% MoM and fell short of our previous estimate due to HDD shortage and inventory correction.

• The company revised down its 4Q11 shipment guidance from 10-15% QoQ decline in September to 30% decline. Our 4Q11 motherboard shipment estimate is in line with company revised guidance of 30% QoQ decline mainly due to the impact of HDD shortage. China demand is seeing a slow down, according to the company.

• We expect January motherboard shipment to drop 17% MoM to 1m units due to Chinese New Year week-long holiday. Our forecast for 1Q12 is 8% QoQ growth, less than the historical average of double-digit QoQ growth partly because demand for high-end motherboards usually comes in 1Q but this time it will probably come only in 2Q12 after the launch of Ivy Bridge because users may delay their purchase.

MicroStar (2377 TT, not rated)

• The company guided for a flat November; we have forecast a 5% MoM growth due to a lower-than-expected October base. December motherboard shipment is estimated to remain sluggish at 1m units. October motherboard shipment came in worse than our previous forecast and the guidance of 10-20% MoM decline due to the impact of HDD shortage in 2H October, according to the company.

• We now expect 4Q11 motherboard shipment to decline 21% QoQ, versus our previous forecast of 17% decline due mostly to HDD shortage which affected the smaller players such as MicroStar more than the bigger ones.

• We expect January to decline 15% MoM due to Chinese New Year, but 1Q12 to grow 20% QoQ due to lower-than-average 4Q11 and normal seasonality.

Elitegroup (2331 TT, not rated)

• We are revising up November motherboard shipment to 1.65m from 1.55m units as HDD shortage appears to have had less impact on the ODM market, where the Elitegroup has a bigger exposure, and better demand from China, according to the company. We expect December to decline to 1.4m units due to a higher-base November, with China remaining relatively stronger than other regions. October came in at 1.5m units, lower than our previous forecast due to a slow down in orders from China after its National day holidays.

• We are now estimating 4Q11 to decline 5% QoQ, worse than our previous forecast of 2% decline due to lower-than-expected October shipment. However, we note that the 4Q11 decline is the lowest amongst the motherboard players due to its higher concentration in the ODM market.

• We expect January to decline to 1.2m units due to Chinese New Year and 1Q12 to decline 11% QoQ as historically 1Q is a low season for the company.

Appendix

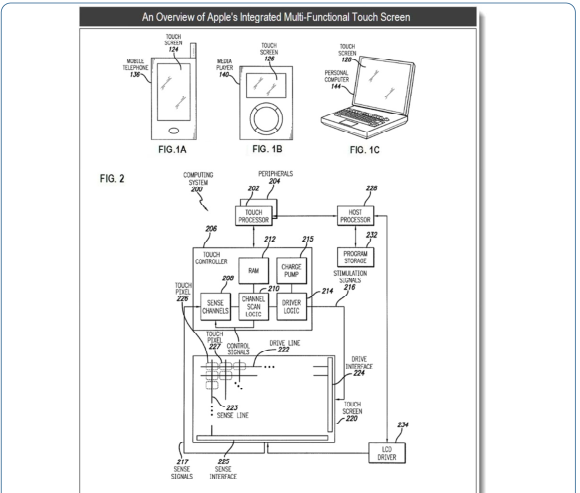

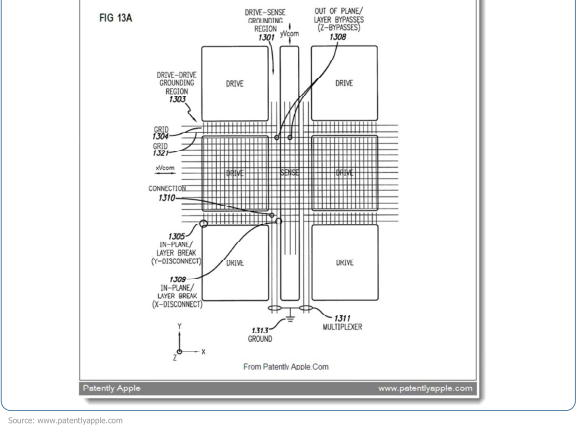

Figure 9. Apple’s Integrated Touch Screen Patent Snapshot

About the Patent Figures: Patent FIGS. 1A-1C illustrate an example mobile telephone, digital media player and personal computer that each include an example integrated touch screen; FIG. 2 is a block diagram of an example computing system that illustrates one implementation of an example integrated touch screen; FIG. 13A illustrates an example configuration of multi- function display pixels grouped into regions that function as touch sensing circuitry during a touch phase of a touch screen.

Apple's Summary: The patent relates to touch sensing circuitry integrated into the display pixel stackup (i.e., the stacked material layers forming the display pixels) of a display, such as an LCD display. Circuit elements in the display pixel stackups could be grouped together to form touch sensing circuitry that senses a touch on or near the display. Touch sensing circuitry could include, for example, touch signal lines, such as drive lines and sense lines, grounding regions, and other circuitry.

An integrated touch screen could include multi-function circuit elements that could form part of the display circuitry designed to operate as circuitry of the display system to generate an image on the display, and could also form part of the touch sensing circuitry of a touch sensing system that senses one or more touches on or near the display.

The multi-function circuit elements could be, for example, capacitors in display pixels of an LCD that could be configured to operate as storage capacitors/electrodes, common electrodes, conductive wires/pathways, etc., of the display circuitry in the display system, and that may also be configured to operate as circuit elements of the touch sensing circuitry. In this way, for example, in some embodiments a display with integrated touch sensing capability may be manufactured using fewer parts and/or processing steps, and the display itself may be thinner, brighter, and require less power.

Source: www.patentlyapple.com

Granted Patent Number 7,995,041

Post time: Dec-23-2019